Stablecoins Will Destroy Trad-Fi

Traditional finance had a good run.

Like the advent of Internet-based banking, a new technological marvel is waiting in the wings as an inevitable disrupter. And it's not something flashy like 'artificial intelligence'; it's the simple concept of stablecoins.

Stablecoins Unlock Micropayments

When was the last time you paid someone $0.003 for something?

Answer: You haven't.

It's not your fault ... you can't. Traditional payment rails - ACH, SWIFT, Visa - carry transaction costs that make micropayments economically unfeasible. Sending ten cents through a bank costs more than ten cents to process.

Stablecoins eliminate that constraint. On modern crypto networks, very small payments are technically and economically rational. This opens entire categories of commerce that cannot exist in traditional finance:

- pay-per-article journalism

- per-second streaming royalties

- machine-to-machine payments in the IoT economy

- real-time freelancer compensation

- AI subscription credits

When the unit of value can be as small as the transaction itself, entirely new business models emerge. And trad-fi's existing cost structure can't support it.

Crypto Rails Are Dirt Cheap - And Nobody Owns Them

We all pay for Visa's network.

You do. Merchants do. Everyone does - through interchange fees, processing fees, and currency conversion markups that take away material amounts of each payment.

Crypto infrastructure is financed differently. Layer-1 protocols like Xahau and Solana fund their networks through validator incentives baked into the protocol itself. The cost isn't heaped onto a corporation that then multiplies it before charging the consumer. Instead, It's distributed across the network infrastructure providers that are focused on meeting the performance requirements to retain their incentives. Competition between validators drives the cost toward its natural floor.

Top Ten USD Stablecoins

Top Ten USD Stablecoins

The result: Transaction fees that are fractions of a cent - for a payment network that is world-wide, 24/7, and permissionless.

- No correspondent bank taking a cut

- No settlement windows measured in "business days"

Traditional financial infrastructure is not just expensive - it's structurally expensive. That's not a problem that can be fixed with better software; It's a consequence of the business model.

Central Banks Want Stablecoins

Programmable money gives regulators tools they've never had before. And no, I'm not talking about the dystopian concept of a 'central bank digital currency' (CBDC).

Consider fractional reserve banking. Right now, banks are legally required to hold a fraction of deposits as reserves and restrict how much risk they can handle. But enforcement is reactive. Regulators audit after the fact, issue fines after the fact, and intervene - if they're lucky - before a contagion spreads.

With tokenized assets on a public blockchain, the rules can be encoded directly into the money. Reserve requirements don't need to be audited - they can be enforced by smart contracts in real time. Regulatory risk limits are measurable instantly, verifiable by all stakeholders.

Customers Already Know What They Want

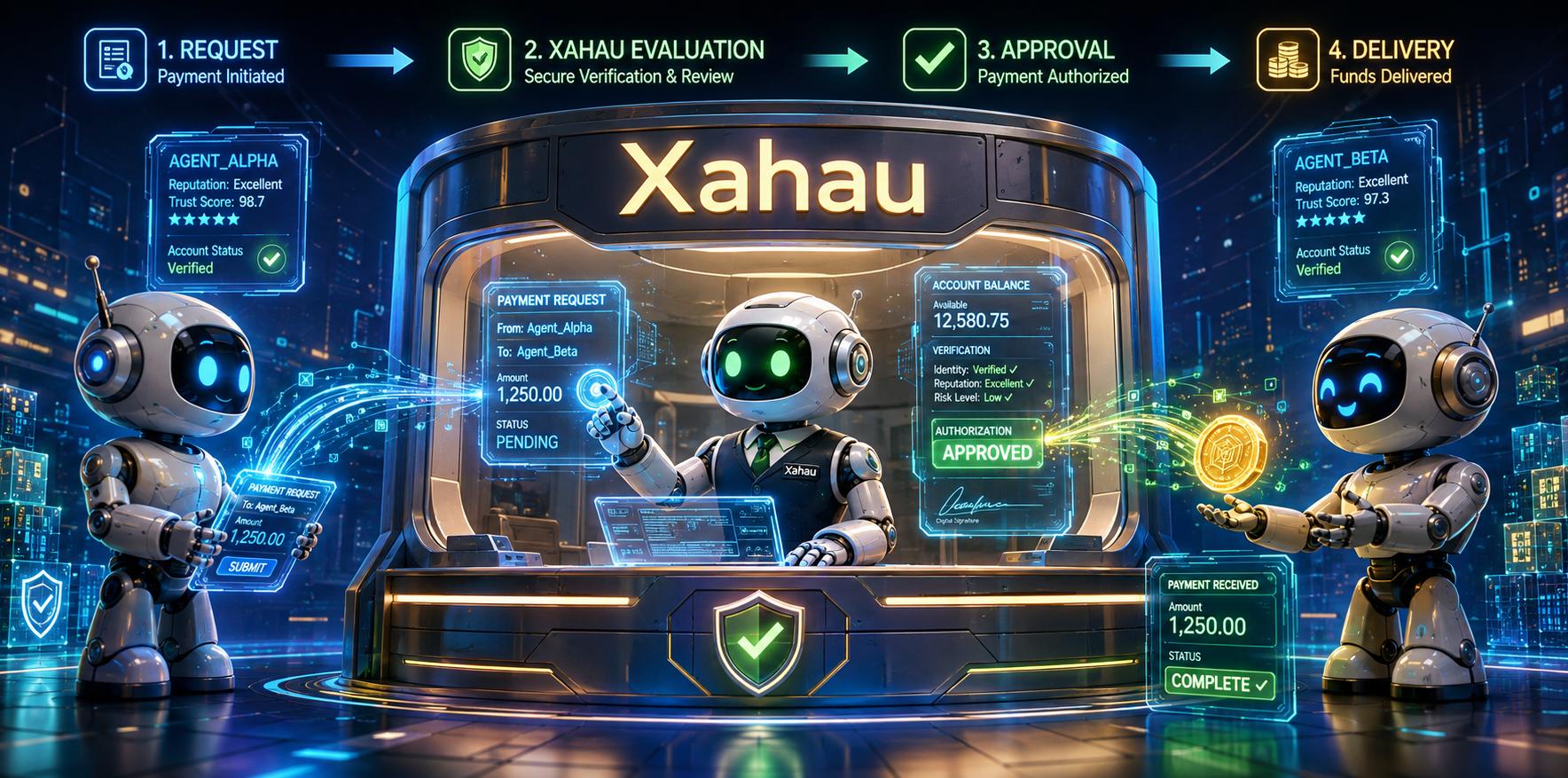

People want to be paid immediately for work done.

Gig workers, freelancers, contractors, and traditional employees share a common problem: you complete the work, and then you wait. Two weeks. A month. The money sits somewhere ... earning interest for others.

Stablecoin payments settle in seconds.

Example: A freelancer in Brazil completes a project for a client in London, and the payment arrives as soon as the work is reviewed. In the crypto world, the client can push a button, releasing an escrowed payment of Euros.

Stablecoin Escrow Release

Stablecoin Escrow Release

This isn't a feature that needs to be sold; it's a feature that sells itself.

Credit Card Processors Know

The headlines were fast and furious throughout the last two years; credit card processors taking the difficult steps to integrate with the new payments rails.

April 2026 Coverage Of VISA By Cryptoslate

April 2026 Coverage Of VISA By Cryptoslate

The Future Belongs to Better Technology

Kodak didn't lose to a better film company. Blockbuster didn't lose to a better video store. They lost to technologies that made the old model unnecessary.

Traditional finance is facing the same structural challenge. It's not that stablecoins are a little better at moving money - it's that they're way, way better.

- Cheaper rails

- Programmable compliance

- Instant settlement

- Worldwide access

- Micropayments

Stablecoins won't destroy traditional finance because they're fashionable. They'll destroy it because they're better.

Sources

https://bitwage.com/en-us/blog/stablecoin-micropayments-unlocking-new-business-models

https://mmc.vc/research/stablecoins-entering-their-untethered-growth-era/

Stablecoins: Growth Potential and Impact on Banking https://www.federalreserve.gov/econres/ifdp/files/ifdp1334.pdf

Visa Tests Stablecoin Payouts to Speed Payments for Creators, Gig Workers https://www.coindesk.com/business/2025/11/12/visa-tests-stablecoin-payouts-to-speed-payments-for-creators-gig-workers